Decarbonizing aviation through low-carbon fuels will be beyond difficult

Blog

Will slow and steady win the race for alternative jet fuels?

The International Civil Aviation Organization (ICAO) relies heavily on the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) to reduce greenhouse gas (GHG) emissions from international aviation. Rather than aircraft technology and operational improvements, ICAO is counting more on airlines switching to alternative jet fuels (AJF) together with purchasing carbon offsets to achieve emission reductions. Is ICAO being overly optimistic, or is decarbonization of the aviation industry really achievable through the use of alternative fuels?

Alternative jet fuel proponents paint a bright and colorful picture of the state of the industry, pointing to several offtake agreements AJF producers have secured with various airlines. While it’s true that airlines seem interested in purchasing AJF, producers have been slow to actually deliver their products. Alternative jet fuel has only been produced on a commercial level in the United States since 2016, and despite hundreds of millions of dollars in support from the U.S. Government, production is not ramping up fast. A list of AJF producing facilities in the U.S., along with the technology pathways they use and their production capacity, is presented in the table below.

| Company | Pathway | Feedstock | Facility Location | Current capacity (gal/yr) | Future capacity (gal/yr) | Notes |

|---|---|---|---|---|---|---|

| AltAir | Hydroproccessed Esters and Fatty Acids (HEFA) | oils (currently tallow) | Paramount, CA | 30-40 M | ~120M | Potential to quadruple today’s capacity, including jet and road fuels |

| Gevo, Inc | Alcohol-to-jet | Sugar-isobutanol | Silsbee, TX; Luverne, MN | 30,000 | 24M | |

| Fulcrum | Fischer-Tropsch | Municipal solid waste | McCarran, NV | N/A | 10M | First refinery began construction in 2018 |

| Red Rock | Fischer-Tropsch | Forest bi-product | Lakeview, OR | N/A | 7M jet, 7M diesel, 4M naphta | Began construction in July 2018 |

| SG Preston | Hydroproccessed Esters and Fatty Acids (HEFA) | Not specified | Ohio | N/A | ~120M | Future capacity including road fuel |

Not all negotiations for offtake agreements between fuel producers and airlines are successful. For example, it’s not clear that Gevo Inc’s agreement with Deutsche Lufthansa AG (Lufthansa) will ever be finalized. The two entered into a heads of terms agreement in which Lufthansa agreed to consider buying 40 million gallons of AJF from Gevo over 5 years. When the negotiation terms were established in September 2016, Gevo was planning to convert their Luverne, MN facility to produce alcohol-to-jet and produce up to 10 million gallons of jet fuel and isooctane annually. However, a year later Gevo’s CEO Pat Gruber admitted in an interview that there was still no definitive agreement with the German airline, partly due to uncertainties in the fuel delivery timeline.

Timely delivery has proven to be a challenge even when an agreement is in place. When Red Rock Biofuels signed offtake agreements with Southwest Airlines in 2014 and FedEx Express in 2015, the company promised the first deliveries would take place two years after the agreements were finalized. Red Rock only began breaking ground for the facility in Lakeview, Oregon this year and revised plans to start operations in 2020. Similarly, SG-Preston promised JetBlue its first delivery in 2019 and Qantas delivery in 2020. It is unclear how the company will meet these dates when it has not commenced construction on any of its facilities.

It’s also not clear if fuel producers will be able to meet their volume targets. Fulcrum BioEnergy established large-volume offtake agreements with several companies, on top of equity acquisition: 375 million gallons for Cathay Pacific, 900 million gallons for United Airlines, and 500 million gallons for Air BP, all over 10 years period. Fulcrum’s first plant, expected to start production in 2020, will only have 10.5 million gallons annual production capacity, or less than 10% what it needs to produce based on the agreements.

AltAir Fuels, the only U.S.-based AJF producer able to deliver AJF and fill its orders, is ahead of its competitors partly because instead of building its facility from the ground up, it was able to convert an existing facility formerly used to produce asphalt. Currently, AltAir is wrapping up a three-year offtake agreement with United Airlines for United’s operations out of Los Angeles International Airport. Although both parties expressed interest in continuing the agreement, there is no indication yet from either party that they will.

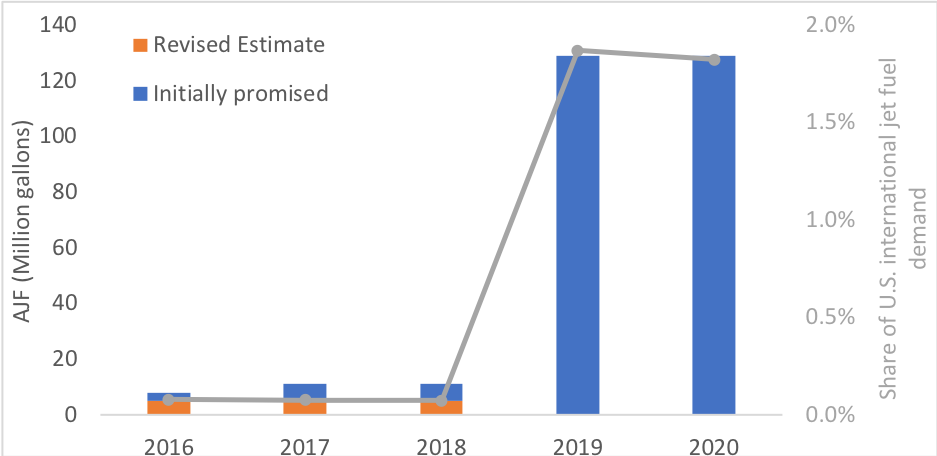

So far, the picture for alternative jet fuels doesn’t look so bright. Currently, only 0.07% of U.S. jet fuel used for international flights is covered by AJF. How would the future for alternative jet fuels look if we optimistically assume new AJF facilities will be built and producers will deliver the promised amount of AJF on time? To find out, we calculated the share of fossil jet fuel that would be displaced through 2020 (chart). Even if all current agreements on fuel delivery were actually met in 2020, which seems unlikely, the portion of aviation fuel made up of AJF would be meager. The best scenario shows no more than 2% of total U.S. jet fuel demand for international flights would be fulfilled by AJF by 2020. Sure, new agreements may be established during this time, but it’s unlikely new projects will produce fuel by 2020.

Currently, the United States is the world’s main petri dish for AJF development and commercialization. Europe, for example, is yet to witness a long-term AJF offtake agreement being fulfilled in the region. At this rate, it seems quite impossible that the aviation industry would reach the “nearly complete replacement of petroleum-based jet fuel with sustainable alternative jet fuel” needed to meet its goal of carbon neutral growth from 2020.