Effective policy design for promoting investment in advanced alternative fuels

Blog

ICAO’s CORSIA scheme provides a weak nudge for in-sector carbon reductions

The International Civil Aviation Organization (ICAO) has not yet figured out how to decarbonize jet fuels. Under the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), approved in June 2018, the international aviation sector is expected to collectively reduce its annual emissions by approximately 2,000 million tonnes of CO2 in 2050 relative to a “business-as-usual” scenario. ICAO anticipates that in the early stages of CORSIA, emission reduction goals will be met through carbon offsetting as the advanced alternative jet fuel industry develops. In later stages, operators are expected reduce emissions in-sector through the use of alternative jet fuels and improved aircraft efficiency. After ICAO’s effort to implement a binding alternative fuel consumption mandate collapsed last year, the long-term deployment of alternative fuels depends on national-level policies and the relative costs of alternative compliance methods such as carbon offsets. But when we take a closer look at the costs of CO2 reductions through these two approaches, it’s not clear that ICAO’s expectation is justified. Does CORSIA really provide a meaningful framework to transition to alternative jet fuels when carbon offsets are both cheap and abundant?

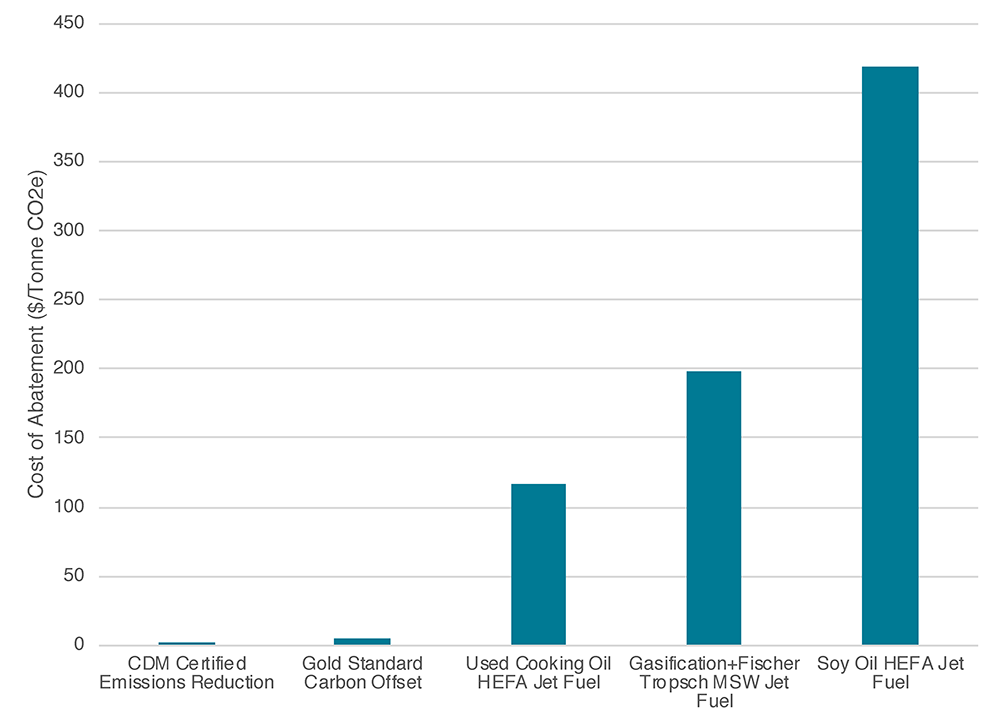

Carbon offsets are a market mechanism to finance emissions reductions. Approved emission reduction projects are awarded credits, which can then be bought and sold on the open market. Carbon offset projects often take place in developing economies with cheaper compliance costs through the purchase of offset agreements by developed countries with climate obligations. The means of generating carbon reductions and the integrity of the offset agreement can vary significantly, with projects ranging from renewable energy deployment to reforestation. The largest source of carbon offsets comes from the United Nations’ Clean Development Mechanism (CDM). The CDM has generated billions of certified emissions reductions (CERs) since its inception, the value of which hovers at less than €1 per tonne of CO2 today. There are currently enough CERs on the market to fulfill CORSIA’s projected demand of 2.7 billion tonnes of carbon offsets through 2035.

While CERs are abundant, their actual GHG impact has been called into question—there is emerging evidence questioning their additionality relative to existing policies. A recent analysis sponsored by the European Commission argues that only 2% of the projects and 7% of CERs supplied have a high likelihood of delivering additional emission reductions that would not have occurred in the absence of the CDM program. A similar analysis suggests that most of the credits available today finance projects that would have happened by 2020 regardless of the offset program, and thus would not provide any additional benefit by the time of CORSIA’s implementation. Despite these risks, countries such as Brazil and China have called for the automatic eligibility of CERs in CORSIA. Efforts to mitigate these risks by narrowing project eligibility beyond 2020 and only certifying projects with a high potential of additional GHG reductions would likely increase the cost of compliance. For example, the price of offsets certified through the more rigorous Gold Standard carbon offset program is over an order of magnitude higher than the typical CER, but still only $4.6 per tonne of CO2e.

Deploying alternative jet fuel can be significantly more cost-prohibitive than purchasing carbon offsets. Economic and political uncertainty, feedstock prices, and technological barriers can make advanced biofuel production challenging and expensive. Consequently, less than 1% of the jet fuel consumed globally comes from alternative fuel producers, with just a handful of production facilities across the world. A recent analysis of production costs estimates that even the cheapest alternative jet fuel pathway is around 50% more expensive than baseline petroleum jet fuel. Normalized in terms of cost per tonne of CO2e abated, the fuel pathways closest to commercialization are far more expensive than purchasing carbon offsets. For example, generating GHG reductions from hydroprocessed esters and fatty acids (HEFA) produced from used cooking oil, a pathway nearing commercialization in both the EU and US, costs approximately 4 to 400 times more than an equivalent offset.

Source: Costs derived from Bann et al. 2017; Carbon intensities inferred from comparable road-sector fuel pathways certified under the California LCFS

Despite ICAO’s efforts, there is little evidence to date to believe CORSIA alone will bring about substantial in-sector decarbonization of the aviation industry. The current supply of carbon offsets provides a much more cost-effective form of carbon abatement for the aviation sector than fuel-switching. If some member states are successful in pushing ICAO to adopt lenient requirements for offsets in CORSIA, it is possible that the existing supply of CERs could swamp any alternative compliance for the first 15 years of the program with little climate benefit to show for it. Restricting the eligibility of offsetting projects within the CORSIA program would ensure the program generates real, meaningful GHG reductions. Implementing stringent additionality requirements and introducing a vintage requirement would reduce the pool of offsets available for CORSIA, potentially significantly increasing their price, although they would likely remain cheaper than the alternatives. Even if ICAO tightens up its criteria for offsets, it is clear that CORSIA is not going to drive a wide-scale deployment of alternative jet fuel.