Press release

Fiscal incentives spurring electric vehicles sales, but in widely divergent ways

Electric vehicle sales worldwide in 2013 approximately doubled from 2012 levels, to about 200,000. But that global trend masks significant variation in sales and growth rates across the major auto markets, according to a study released today by the ICCT.

Download “Driving Electrification: A global comparison of fiscal incentive policy for electric vehicles” [.pdf].

The study, which details differences in the fiscal policies used to support electric vehicle sales across eleven major auto markets (eight European countries, China, Japan, and the United States), demonstrates clearly that tax exemptions and subsidies are playing a key role in spurring electric vehicle markets. Norway and the Netherlands, in particular, are conspicuous examples of the relationship between fiscal incentives and electric vehicle sales.

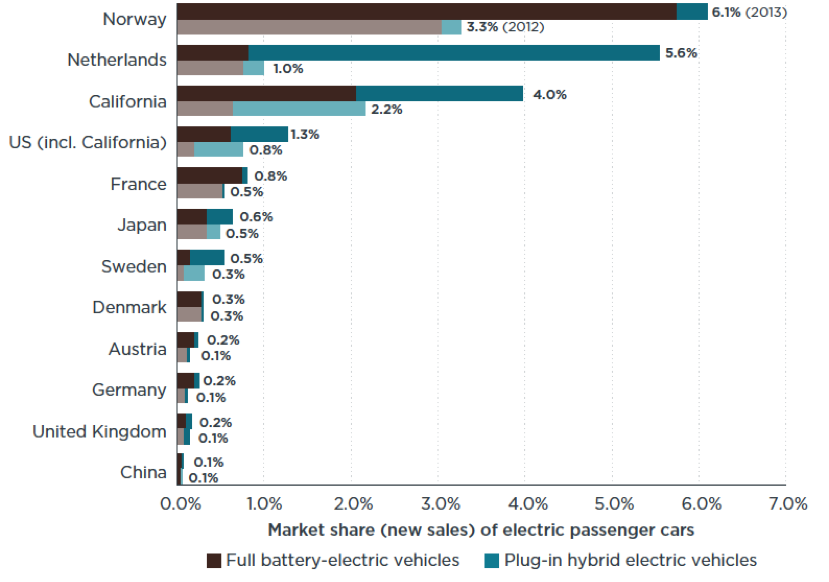

Market share of electric passenger cars for the years 2012 (lighter colors) and 2013 (darker colors), in comparison to total sales

At the same time, the study results show that a number of factors in addition to fiscal incentives are influencing development of the market for electric vehicles. California, especially, exemplifies a comprehensive electric-drive strategy that goes beyond fiscal incentives.

Numbering only in the thousands of units globally in 2009, electric vehicle sales worldwide have approximately doubled in each of the past couple years, reaching 200,000 in 2013. Relative to the tens of millions of vehicles coming to the market each year, of course, the fraction of electric vehicles is still tiny.

But in some regions electric vehicle sales are becoming a more significant proportion of total sales, as the recent inventory by the ICCT shows. Norway is the global frontrunner, with electric vehicles accounting for about 6 percent of all new car sales. Closely following Norway is the Netherlands, with a 5.6 percent sales share, and California, at 4 percent. All three markets also show high growth rates: in Norway and California the number of electric vehicles sold doubled in 2013 compared to the previous year, and in the Netherlands there were six times more electric vehicles sold than in 2012.

Germany and the UK, in contrast, are among the slower electric vehicle markets, with only about 0.2 percent of all new sales being electric.

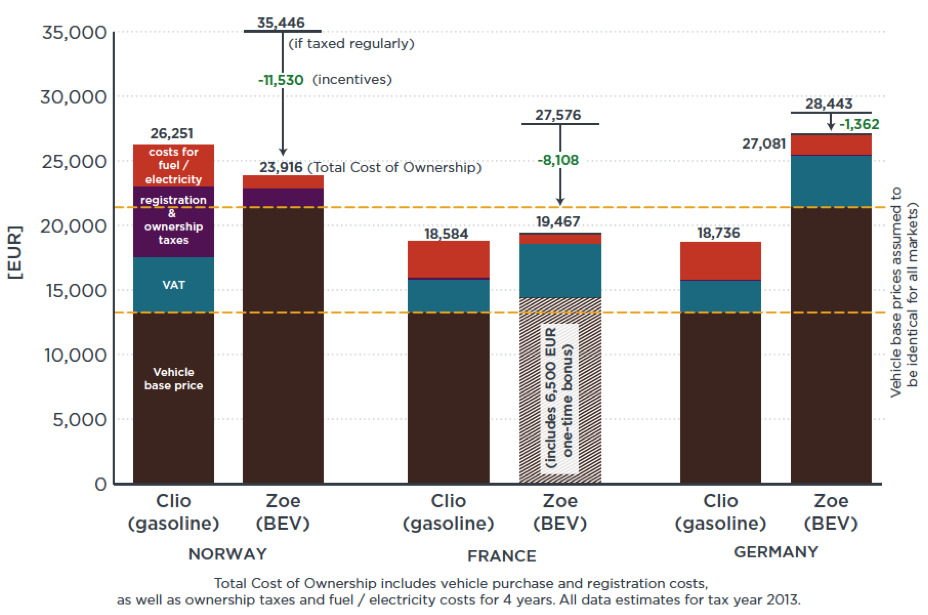

Comparison of total cost of ownership for a Renault Zoe battery electric vehicle and a Renault Clio gasoline vehicle for Norway, France, and Germany.

The ICCT study is a novel, comprehensive international comparison of fiscal incentives for electric vehicles in eleven large automobile markets. The assessment compiles data from government and industry sources on overall vehicle sales, plug-in electric vehicle sales, vehicle taxation policy, vehicle taxation exemptions, and electric vehicle subsidies. Furthermore, it takes into account differences in prices for fuel and electricity in the respective countries.

The results demonstrate that there are large differences in the level and type of fiscal incentives for electric vehicles across the markets. The incentive provided by Dutch government, for example, on a typical plug-in-hybrid electric vehicle amounted to approximately 38,000 Euro ($52,000) per vehicle, or nearly three-quarters of the vehicle base price. That incentive took the form of full exemptions from registration and annual vehicle taxes. In Germany, by contrast, owners of electric vehicles ended up paying more taxes than they would have owed on comparable non-electric combustion engine vehicles, as the minimal current tax exemptions offered there are more than fully offset by the higher value-added tax (VAT) that generally applies to electric vehicles.

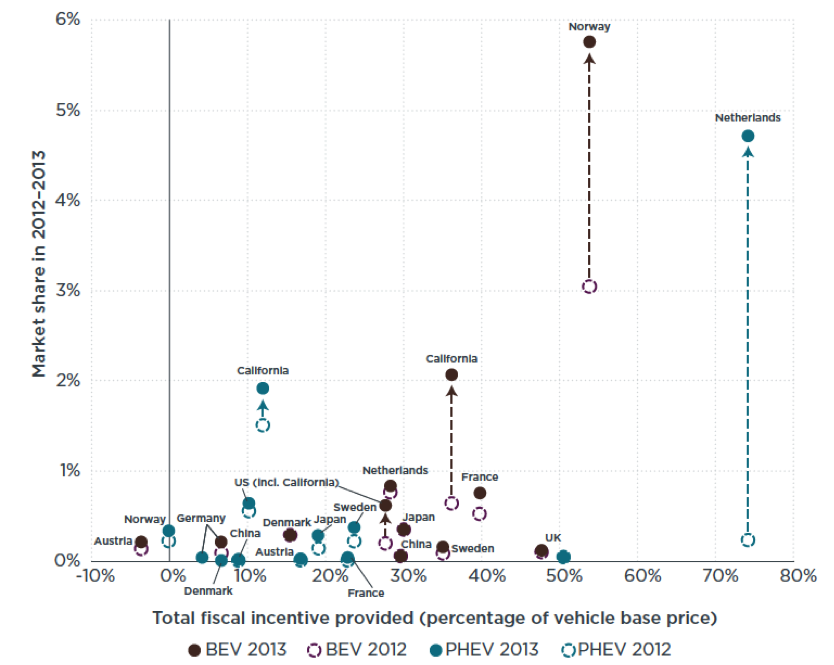

The correlation between fiscal incentives and electric vehicle sales is clear in some cases. “Norway and the Netherlands are good examples of markets where high levels of fiscal incentives lead directly to high numbers of electric vehicles sales,” says Dr. Peter Mock, Managing Director of ICCT Europe and one of the authors of the study. But in other instances a definitive connection between incentives and sales conclusion is much more elusive. “A counter-example is the UK, where despite relatively high incentives electric vehicle sales are still very low,” said Mock.

2012 and 2013 market share of passenger cars vs. per-vehicle incentive for battery electric (BEV) and plug-in hybrid electric (PHEV). The incentive provided is shown as percentage of vehicle base price to allow for a comparison across vehicle segments.

There is no question that fiscal incentives and differences in fuel and electricity prices do not tell the full story. Other factors are playing an important role in promoting electric vehicles, as well. California offers the prime example. The level of fiscal incentive there is only about average when compared to other main markets worldwide. However, electric vehicle sales are well above average, and California has a more comprehensive electric vehicle deployment plan that includes vehicle manufacturer policies (e.g., CO2 standards, electric vehicle requirements), charging infrastructure investments, electric utility actions, consumer awareness campaigns, and other local initiatives. Better understanding the importance of these factors that go beyond fiscal policy could help to explain the variation in electric vehicle sales across world auto markets.