Oil market futures: Effects of low-carbon transport policies on long-term oil prices

Blog

Policies for efficient transport will lower oil prices, create jobs, and help countries meet climate pledges

Signed by 177 countries in April, the Paris climate agreement has been hailed by business leaders and heads of state as the “end of the fossil fuel era.” Now, as countries translate their intended nationally determined contributions into domestic actions, we can expect to see the development of low-carbon policies at an unprecedented scale. In the transport sector, responsible for about one quarter of anthropogenic carbon dioxide emissions and the majority of petroleum consumption, the adoption of low-carbon transport policies has already been accelerating for several years. Today, 83% of new passenger car and light truck sales worldwide are covered by fuel-efficiency regulations. The United States, China, Japan, and Canada, which together account for half of all new heavy-duty vehicles (HDVs) sales worldwide, have also adopted fuel-efficiency regulations covering those vehicles. Two other major vehicle markets, the European Union and India, are working to adopt comparable efficiency regulations as well; when they do, 63% of global sales of HDVs will be subject to fuel-efficiency standards.

This expansion of fuel-saving transport policies has important implications for the future of the global oil market and its impacts on major economies, which we’ve recently outlined in a study we did with Pöyry Management Consulting and Cambridge Econometrics.

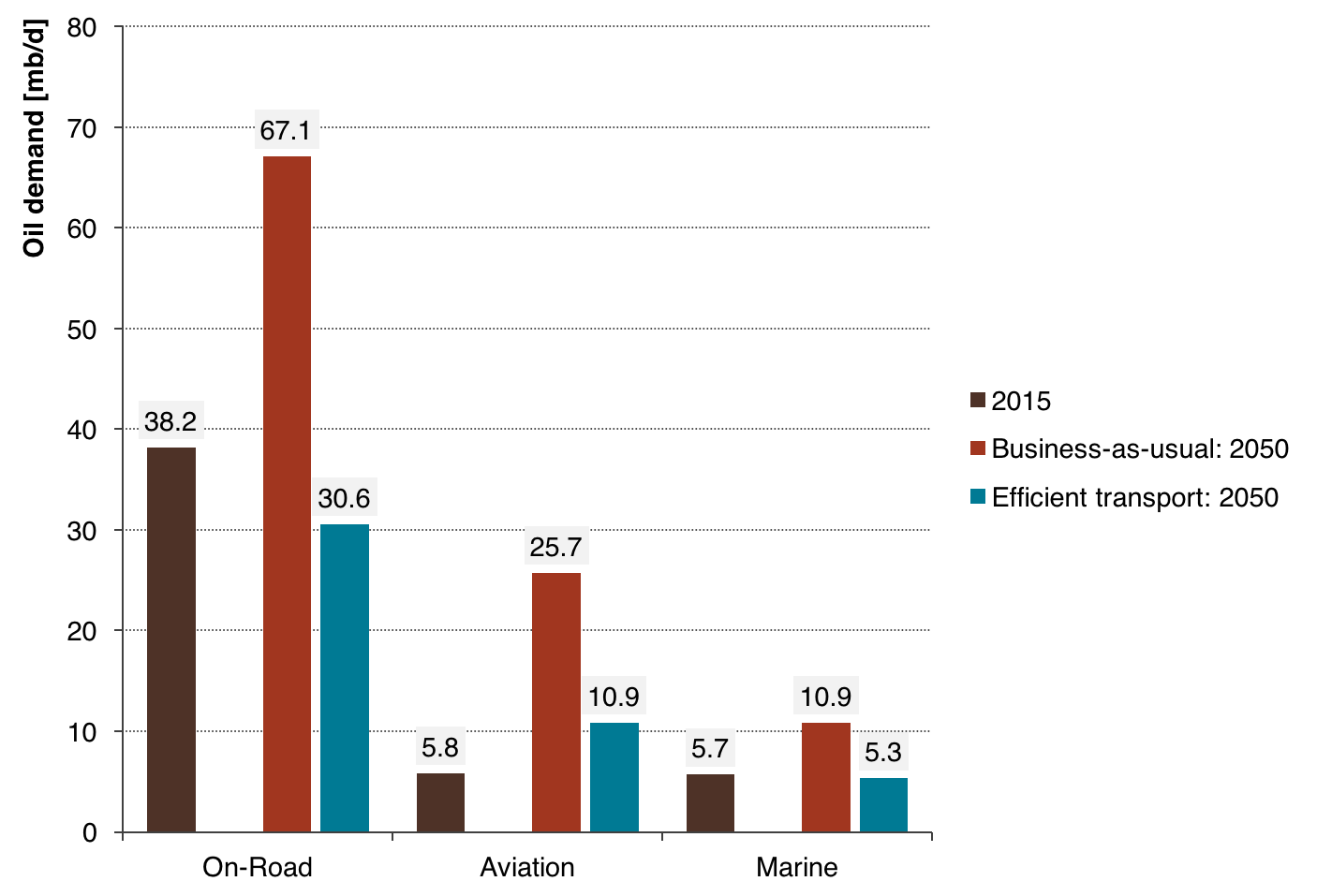

In a business-as-usual scenario, assuming present market trends continue and no additional fuel-saving policies were adopted, oil demand in the transport sector could double between now and 2050, driven by growth in the demand for passenger and freight services. While about half of this new oil demand is expected to come from on-road vehicles, the other half could take place in the aviation and marine sectors. To put this into perspective: if all sectors were to experience similar levels of growth in energy demand and associated greenhouse gas emissions, this business-as-usual scenario would fall among the 90th percentile (highest) of emissions scenarios considered by the IPCC’s Fifth Assessment Report.

However, fuel-saving policies in the transport sector could radically alter that outcome. Expanded adoption of domestic policies that promote passenger and freight vehicle efficiency (including next-phase standards in countries with existing fuel-efficiency standards) and transition passenger vehicle fleets to electric-drive vehicle technologies, combined with international measures that improve the efficiency of new and operating aircraft and marine vessels, could stabilize transport sector oil demand near 2015 levels in 2050.

Figure 1. Global oil demand from transport in 2015 and under two scenarios for 2050

This stabilization of transport oil demand could put transport sector greenhouse gas emissions on a similar pathway as economy-wide emissions according to the pledges made by countries under the Paris agreement, which the Climate Action Tracker Partners estimate would translate to economy-wide emissions in 2050 that are near 2015 levels.

But a stabilization of transport oil demand also has far-reaching economic implications in addition to its environmental benefits. Presently, the price of oil can be expected to recover to between $80/bbl and $90/bbl within a decade as the current environment of excess supply transitions to a market equilibrium; already, declining investments in oil production are raising concerns of a sharp oil price rebound toward the end of the decade, according to the International Energy Agency (IEA). Under a business-as-usual scenario, the price of oil could climb to $130/bbl in 2050. Such a scenario would be unfavorable for both consumers and countries seeking to follow through on their climate pledges.

Figure 2. Cost of oil production under business-as-usual and efficient transport scenarios

In contrast, stabilizing oil demand in the transport sector could keep long-term oil prices below $90/bbl, a reduction of $40-50/bbl compared business-as-usual in 2050. And at prices below $90/bbl, investments in Arctic and ultra-deepwater oil sources are uneconomical. Recent actions by oil companies to abandon Arctic oil exploration rights evidence the impact of lower oil prices on divestment from high-cost production.

While an efficient transport scenario may appear gloomy to high-cost oil producers, it looks great for consumers and the wider economy, especially in oil-importing regions. In Europe, for example, the reduction in oil prices from efficient transport policies could save consumers billions of dollars, add 400,000 service sector jobs in 2050, and increase GDP by half a percentage point as a result of the increase in consumer income and spending. And these benefits don’t even capture the returns on investments in fuel-saving technologies and electrified transport, nor do they include the reduction in fuel costs for international marine freight and commercial aviation providers.

So as countries translate their climate pledges into concrete action in the coming months, remember that climate benefits aren’t the only benefit at stake. For the transport sector, policies that promote efficiency are also a mechanism to lower oil prices, create jobs, and grow the economy.