Heavy fuel oil is considered the most significant threat to the Arctic. So why isn’t it banned yet?

Blog

The end of the era of heavy fuel oil in maritime shipping

Since the 1960s, heavy fuel oil (HFO) has been the king of marine fuels. Viscous, dirty, yet inexpensive and widely available, HFO propelled a long period of robust growth in international shipping, which carries over 90% of intercontinental trade by volume each year. For many, it is the lifeblood of the maritime shipping industry.

But HFO’s low price does not reflect its impacts on the environment and human health. The sulfur content of HFO can be up to 35,000 parts per million. It is the reason that maritime shipping accounts for 8% of global emissions of sulfur dioxide (SO2), making the industry an important source for acid rain as well as respiratory diseases. In some populous port cities, such as Hong Kong, shipping is the largest single source of SO2 emissions as well as emissions of particulate matter (PM), which are directly tied to the sulfur content of fuel. By one estimate, PM emissions from maritime shipping led to 87,000 premature deaths worldwide in 2012.

The International Maritime Organization (IMO), the governing body of international shipping, has made a decisive effort to diversify the industry away from HFO into cleaner fuels with less harmful effects on the environment and human health. Effective in 2015, ships operated within the Emission Control Areas (ECAs) covering the Economic Exclusive Zone of North America, the Baltic Sea, the North Sea, and the English Channel will begin to use Marine Gas Oil (MGO) with allowable sulfur content up to 1,000 ppm. Starting from 2020, ships sailing outside ECAs will switch to Marine Diesel Oil (MDO) with permitted sulfur content up to 5,000 ppm.*

That tectonic shift also creates openings for a variety of new fuels. Liquefied nature gas (LNG), newly abundant and relatively affordable, is attracting the attention of many shipping companies. Although the lack of infrastructure and the uncertainty of future prices have slowed the “dash to gas,” many expect LNG to establish itself as one of major alternatives to HFO in the future. Lloyds Registry, a shipping classification society, expects LNG to take 11% of the market share in 2030. Meanwhile, Stena Teknik, a Swedish company, is testing methanol, another natural gas product, but one that requires less storage space in a ship and is relatively easier to handle. While natural gas-based fuels may sometimes offer questionable climate benefits, due to methane leakage concerns, the IMO’s low-sulfur regulation may create needed openings for other zero-sulfur, low-carbon marine fuels. Tests using fuel cells on the Viking Lady, an offshore supply ship, demonstrated promising results. Wind kites and solar panels have already been installed on numerous ships to supplement marine diesel engines. Even HFO will not completely disappear from the menu of marine fuels. Combined with scrubbers that capture more than 99% of the sulfur from the exhaust gas, HFO will continue to play an important role. Lloyds Registry reckons that HFO will represent about 40% of fuel use by 2030.

The shift to cleaner but pricier low-sulfur fuels is likely to heighten interest in the “fifth fuel”: energy efficiency. Historically, the maritime shipping industry, where energy often accounts for over half of operating costs, has responded to escalating fuel prices with innovative energy-saving strategies. To cite a recent example: in 2008, as fuel prices went through the roof, shipping lines cut their operating speeds by as much as 50%, helping many companies stay afloat amid one of the worst downturns in history. In an analysis of satellite data on ship operations, we’ve estimated that the industry can further slash 100 million ton of fuel use by 2030 through wider implementation of energy-saving measures that were adopted by industry leaders in 2011. This is in addition to savings of 90 million tons of fuel because of the Energy Efficiency Design Index (EEDI), a mandatory program that will require new ships to achieve certain efficiency targets beginning in 2015.

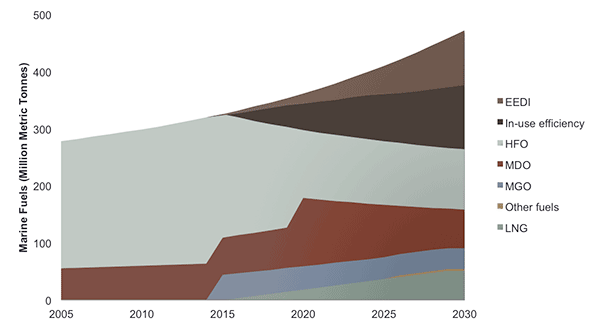

The continued diversification of marine fuels and improvements in energy efficiency have important implications. First and foremost, they may alleviate concerns about the availability of low-sulfur fuels. Figure 1 illustrates one possible scenario, using our forecast on future marine fuel consumption and energy efficiency improvements as well as Lloyds Registry’s estimate of market shares for HFO and LNG. The efficiency improvement of the legacy fleet is the greatest force driving down the need for low-sulfur fuels, equivalent to adding about 110 “negatons” of fuel, or almost 24% of projected demand. HFO combined with scrubbers, EEDI, and distillates (MGO plus MDO) are almost neck and neck, each representing about 20% of fuel use in the chart. LNG is coming of age, with its share doubling between 2020 and 2030. Other fuels, such as renewables, fuel cells, and biofuels, are expected to hold only small market shares in 2030.

Marine fuel use, 2005–2030

Second, the new fuels are on a collision course with IMO safety regulations concerning flashpoint, the temperature at which a fuel can vaporize to form an ignitable mixture in air. The IMO currently requires marine fuels to have a minimum flashpoint of 60°C. But low-sulfur fuels have a lower flashpoint (50° to 55°C), meaning that they are “off-spec” and cannot be used under the IMO rule. The flashpoint requirement, which went into effect in 1976, was meant to provide a large margin of error to ensure the temperature of the engine room (normally below 45°C) does not exceed the flashpoint in any circumstance. But according to industry heavyweights such as Maersk and BIMCO, modern technologies such as advanced ventilation systems provide an adequate safety margin, and they argue that keeping the flashpoint requirement will cause the industry to miss the opportunity represented by the increased availability of low-sulfur, low-flashpoint fuels. Industry and member states such as the U.S. are urging the IMO to accelerate its consideration of an amendment to the flashpoint requirement.

*Implementation of the requirement is subject to a review of fuel availability to be completed by 2016.