Blog

Airline efficiency: Waiting for ICAO?

The gap between the most fuel-efficient and least fuel-efficient airlines on U.S. domestic operations stayed rock-steady at 26% from 2010 to 2012. Meanwhile, overall industry fuel efficiency improved about 1.1% per year—short of both the 1.5% annual improvement the U.S. government assumed in its aviation greenhouse gas emissions (GHG) reduction plan [.pdf] or the 2% aspirational fuel efficiency goal [.pdf] ICAO has established for international aviation. To put this in context, some other transport modes are now demonstrating 6%+ annual improvements in new vehicle efficiency due to public policies.

The numbers are not trivial. In the U.S., aviation accounted for about 11% of energy-related carbon dioxide emissions from the transportation sector (4% of the U.S. total) in 2010. Globally, aviation greenhouse gas emissions are rising 3% to 4% annually, and are expected to quadruple by midcentury if present trends continue.

Conventional wisdom holds that fuel-efficient technologies and practices are rapidly adopted by the aviation industry to reduce the impact of high fuel costs. In fact, our updated U.S. airline fuel efficiency ranking [.pdf] found a weak link between efficiency and profitability in 2012. While efficient carriers like Alaska and Spirit invest in fleet efficiency and operational improvements, the least efficient carrier, Allegiant, and increasingly Delta, are able to reap high profits by operating older, cheaper aircraft.

There is a trade-off between financial and environmental costs, with some airlines choosing the latter. For example, airlines may choose to load more fuel than required (“tanker”) because the fuel is cheaper at certain airports and/or to reduce turnaround time at the flight’s next stop. But this results in heavier aircraft, in turn causing additional fuel burn.

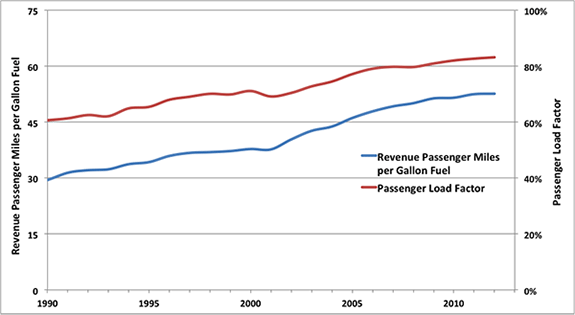

Alarmingly, we see evidence that fuel efficiency improvements in the U.S. aviation market have been slowing down just as climate pressures are speeding up. The figure below shows that efficiency improvement rates (on a revenue passenger mile, RPM, per gallon of fuel basis) were much lower in recent years. The fuel efficiency of U.S. domestic operations improved strongly from 1990 to 2008 – an average of 3% per year – due to improvements in new aircraft efficiency and rising load factors (percentage of seats filled). In recent years gains from new aircraft in the U.S. have fallen, raising the risk that efficiency improvements will stall completely as the marginal gains of filling every available seat drop off.

System-wide fuel efficiency and passenger load factor trends for U.S. domestic passenger operations, 1990–2012. Note: Data represents scheduled carriers, excluding cargo and charter. (Source: Data Base Products, Bureau of Transportation Statistics, Form 41 Financial [2014]).

We first identified the trend of falling improvement for new equipment back in 2009. It’s driven by a lack of new types and by prioritization of aircraft performance, notably range and speed, over fuel burn improvements. Due to the time lag between new aircraft delivery and penetration into the in-use fleet, this slowdown is now evident at the airline level. Since that 2009 report, new aircraft types like the 787-8 have been brought into service, and manufacturers have announced a number of project aircraft (e.g. A320neo, 737 MAX, 777X) that may eventually start to reverse this trend. On top of these improvements, the UN’s International Civil Aviation Organization (ICAO) has projected that the business-as-usual rate of efficiency improvement for new aircraft can be almost doubled* through 2030 given sufficient regulatory and environmental pressure. So what levers are international policymakers going to pull to make this happen?

Nothing quickly, unfortunately. ICAO, the de facto regulator of airlines worldwide, is developing standards and guidelines to improve the environmental performance of aviation. Since the European Union decision to include aviation in its Emissions Trading Scheme (EU ETS) in 2008, ICAO member states have been working towards a framework for a global market-based measure (MBM) as an alternative to limiting the growth of international aviation emissions—but slowly. In October of last year, ICAO convened its 38th Assembly and “decided to decide” upon a global MBM for international aviation in 2016, with possible implementation in 2020. In addition, ICAO is expected to deliver a global CO2 efficiency standard for new aircraft by 2016, although the scale and ambition of that effort are in doubt. In any event, any international policies to address aircraft emissions would not take effect until 2020 or later.

Given the global 4.5% per annum growth in aviation demand and the slow progress in establishing global measures for reducing aviation emissions, meeting the ICAO goal of carbon-neutral growth from 2020 may require a full court press, including global, regional, and even local (i.e. airport-based) measures. If ICAO cannot come to an agreement on a global aviation emissions scheme by 2017, the EU will “restart the clock” to include intercontinental flights (originating or arriving in the EU) in the EU ETS. Simultaneously, the U.S. Environmental Protection Agency (EPA) is expected to release an endangerment finding determining whether greenhouse gas emissions from aircraft endanger human health and welfare and should therefore be regulated domestically under the Clean Air Act, as it already does for cars and trucks. If ICAO cannot develop global measures fast enough, or ambitious enough, to address aviation emissions growth, those regional measures might again come front and center.

*Doc 9963 — Report of the Independent Experts on the Medium and Long Term Goals for Aviation Fuel Burn Reduction from Technology. 2010. 70 pp. ENGLISH ISBN 978-92-9231-765-2 (no hyperlink)